Interest-only mortgage calculator

🏠 Calculate interest-only payments, balloon principal at maturity, and the full schedule for interest-only mortgages (IO loans).

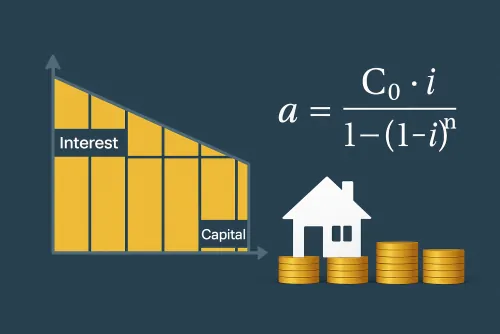

What is the American amortization method?

This interest-only mortgage calculator doubles as an interest-only loan calculator, an American amortization method calculator and even a bullet loan calculator. All of them describe the same structure: you pay only the interest each month while the principal stays untouched until maturity, when you repay it in one lump sum.

The monthly payment is simply the annual rate divided by twelve and multiplied by the outstanding balance. Because the balance never shrinks, the interest-only mortgage payment remains flat and predictable during the entire term.

How to use the interest-only mortgage calculator

Enter the loan amount, annual interest rate and term to let this interest only home loan calculator estimate monthly interest, final balloon payment and total cost. You can tweak the inputs as many times as you want to compare scenarios and understand how each variable affects the schedule.

Use this interest-only mortgage calculator to estimate your monthly interest payments and the final balloon payment with the American amortization method. Enter loan amount, interest rate and term to see the full amortization schedule.

Loan summary

Principal: $0.00

Monthly interest payment: $0.00

Balloon payment: $0.00

Total paid: $0.00

Total interest: $0.00

Values are rounded to two decimals. In the American method the principal is repaid at maturity.

| Month | Payment | Interest | Principal | Balance |

|---|---|---|---|---|

| Complete the form to generate the amortization schedule. | ||||

Once you run the numbers you'll see the breakdown between total interest and principal.

Pros and cons of an interest-only loan

The main benefit is that your monthly cash flow improves because installments consist only of interest. This makes the structure attractive for investors waiting to sell an asset or receive a large inflow. The drawback is the sizeable balloon payment: you need to plan ahead to accumulate the funds on time.

Use the American amortization method calculator periodically to stress test your assumptions and decide whether early principal reductions or savings goals are required.

Example of a loan with the American method

Consider a $120,000 loan at 5 % for 4 years. The interest-only mortgage payment is $500 per month and, at maturity, you repay the $120,000 balloon. If you make a $20,000 partial payment after year two, the remaining monthly interest drops to $333.33 because the balance falls to $80,000.

This example shows how even a small reduction in principal lowers interest expense immediately.

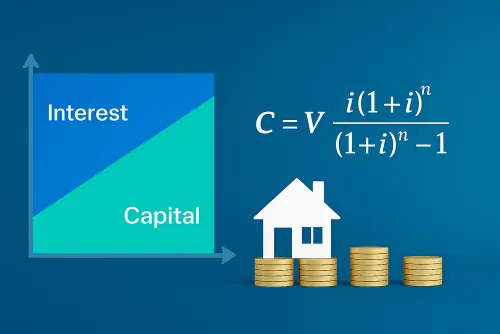

Differences between French, German and American methods

The French method mixes principal and interest in equal installments, the German method amortizes a fixed amount of principal plus declining interest, and the American method keeps the principal untouched until the end. Choose the structure that best matches your income pattern and risk tolerance.

What is an interest-only loan with the American method?

It is a structure where you pay only interest during the term and repay 100 % of the principal as a lump-sum balloon payment at maturity.

When is the American amortization method usually used?

It is often used for short-term financing, bridge loans or mortgages that expect a large cash inflow before maturity.

How are interest payments calculated in an interest-only loan?

The monthly interest equals the outstanding balance multiplied by the annual rate divided by twelve, so the payment remains constant.

What is the difference between an interest-only American loan and a French mortgage?

The American loan charges interest-only installments and repays the principal at the end, while the French mortgage amortizes the balance gradually with each blended payment.

What are the risks of an interest-only loan with a balloon payment?

You enjoy lower monthly payments, but you must be able to save or refinance the entire principal when it comes due.