Decreasing payment mortgage

🏠 Calculate a constant-principal mortgage: decreasing payments over time, interest breakdown, and full monthly schedule.

Decreasing-payment mortgage calculator (German amortization system)

Simulate your decreasing-payment mortgage

This tool is a decreasing-payment mortgage calculator built on the German amortization system. It lets you explore how a constant principal repayment produces declining instalments and shows the full amortization schedule, monthly payments, and total interest at a glance.

Loan summary

Loan principal: 0.00

First payment: 0.00

Total paid: 0.00

Total interest: 0.00

Figures are rounded to two decimal places. Following payments decrease each month under the German amortization method.

| Month | Payment | Interest | Principal | Remaining balance |

|---|---|---|---|---|

| Fill out the form to generate the amortization table. | ||||

Once you calculate your payment you'll see the split between interest and principal here.

What is a decreasing payment and the German amortization system?

A decreasing mortgage payment means you repay a constant amount of principal each month while the interest portion drops because it is charged on a steadily shrinking balance. This produces amortization schedules with a clear view of how much principal is paid off every month.

The German amortization system is a technical framework with constant principal amortization and interest recalculated on the outstanding balance every period. It delivers a transparent amortization table that makes it easy to compare total costs and track how quickly equity builds.

How are payments calculated under the German system?

The principal component is fixed by dividing the loan amount by the number of instalments. For every month, interest equals the remaining balance multiplied by the monthly rate (annual nominal rate divided by 12). Adding both figures gives the payment for that month, which decreases over time.

Advantages of decreasing payments

- Lower total interest because the outstanding balance falls rapidly.

- Monthly cash flow eases over time as the payment decreases.

- Clear amortization schedule that helps with budgeting and long-term planning.

Drawbacks and risks

- Higher initial payments demand more income at the start of the loan.

- Less predictable budgeting if your salary is expected to drop in the future.

- Not ideal when you expect to refinance soon, because the early effort may not pay off.

How to use the decreasing-payment mortgage calculator

This simulator works like a German-system mortgage calculator that highlights the constant principal component and the decreasing payment. Follow these steps before reviewing the amortization table.

- Enter the loan amount you want to finance.

- Enter the annual nominal interest rate.

- Enter the term in years so the tool can convert it to months.

- Click the calculate button to generate the schedule.

- Read the table to see principal amortized, interest, the decreasing total payment, and the remaining balance month by month.

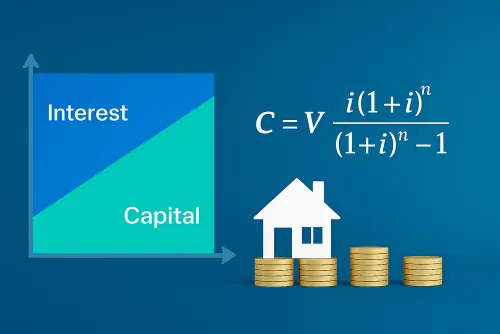

Differences between the French and German systems

Understanding the difference between the French and German mortgage systems helps you decide which model fits your finances. Both repay the loan in full, but the way they distribute principal and interest is distinct.

-

French system

- Fixed payment throughout the life of the mortgage.

- Higher interest portion during the early years.

- Most commonly used in standard home loans.

-

German system

- Constant principal amortization every month.

- Payment decreases steadily as interest charges shrink.

- Lower total interest in exchange for higher upfront payments.

Frequently asked questions about decreasing payments

What is a decreasing-payment mortgage?

It is a loan where you repay a fixed slice of principal every month and the interest portion declines, so the instalment gets smaller over time. The amortization schedule highlights the constant principal and the faster drop in outstanding balance.

How does the German amortization system work?

It keeps the principal repayment constant and recalculates interest on the remaining balance every month. The result is a transparent amortization table with declining payments that shows exactly how much capital you are paying back.

When does a decreasing-payment mortgage make sense?

It suits borrowers who can handle higher payments during the first years and want to reduce their debt quickly. It is also useful when you expect your income to stay steady or grow while you plan to cut total interest paid.

Do I pay less interest than with the French system?

Yes, total interest is usually lower because the outstanding balance falls faster. However, you must be comfortable with the heavier effort at the beginning compared with a fixed-payment French mortgage.

Why are the first instalments higher?

The first payment includes the constant principal share plus interest calculated on the full initial balance. As the balance shrinks, the interest portion declines and so does the total payment.

Can I use this calculator for other loans?

You can apply the same German system to personal, business, or investment loans with decreasing payments. Just enter the principal, rate, and term to obtain the amortization schedule.

How is the amortization schedule generated?

The tool divides the principal by the number of instalments to get the constant amortization and adds the interest for each month. That produces a detailed table with principal, interest, payment, and remaining balance.