Mortgage prepayment to reduce loan term

🏠 Model a partial prepayment to shorten the term: new end date, interest savings, and side-by-side amortization schedules.

This early repayment calculator shows how a lump-sum payment aimed at reducing the term shortens your mortgage or loan while keeping a similar instalment. It works as an amortization simulator focused on shortening the payoff horizon, estimating interest savings and updating the amortization schedule before and after the extra payment.

Early repayment simulator to shorten your mortgage term

This mortgage amortization simulator compares two scenarios: keeping the loan as it is or applying an early repayment focused on reducing the term. It recalculates how many years or months are left and highlights the total interest savings obtained by keeping the instalment steady.

Alongside the new term, the calculator builds the amortization schedule and table before and after the lump-sum payment, so you can clearly see how the payoff date moves forward.

New term: 0 payments

Time saved: 0 payments

Estimated payoff date: -

Interest remaining after prepayment: 0.00

Total interest saved: 0.00

Calculations assume you apply the extra payment today and continue with the same instalment.

Before-and-after comparison

| Item | Before | After |

|---|---|---|

| Payments remaining | - | - |

| Total paid | 0.00 | 0.00 |

| Total interest | 0.00 | 0.00 |

Once you calculate, this chart will show how many instalments you save.

| Period | Instalment | Interest | Principal | Balance |

|---|---|---|---|---|

| Complete the form to generate the updated amortization schedule. | ||||

How to use the calculator to shorten your mortgage

- Enter the outstanding balance, annual nominal interest rate and remaining term of your mortgage or loan.

- Add the lump sum you plan to allocate to early repayment or partial prepayment aimed at reducing the term.

- Run the calculation to see the shorter term, the new estimated payoff date and the interest savings.

- Review the amortization table and schedule to confirm how quickly the principal decreases after the prepayment.

Early and partial repayments focused on reducing the term

An early repayment is an extra payment made directly to the principal. When you keep the instalment steady to shorten the loan, you are performing a partial prepayment designed to reduce the term and maximise interest savings.

With each simulation you can measure how much time you will shave off the loan, how the amortization schedule changes and how much interest you will avoid compared with the original plan.

This mortgage amortization calculator lets you run multiple scenarios instantly, helping you decide the best timing for your early repayment strategy.

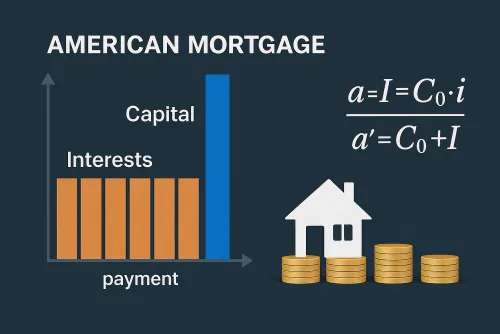

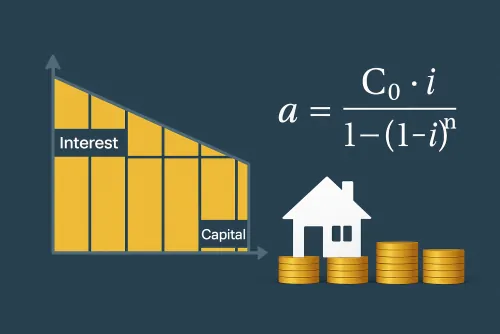

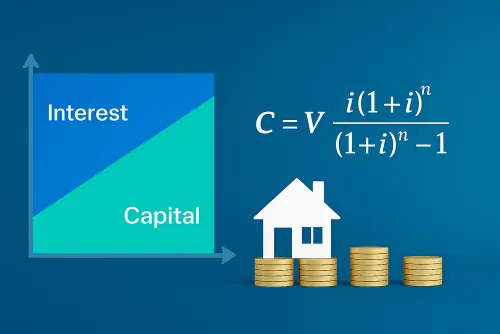

Amortization systems and reducing the term

Most mortgages follow the French amortization system, also known as fixed instalments with a gradually decreasing interest share. Our simulator respects this structure to show the impact of a lump-sum payment.

When you prepay, you can choose between reducing the term or lowering the instalment. This tool focuses on term reduction. If you need to cut the monthly payment instead, there is a separate calculator dedicated to that goal.

The tool rebuilds the amortization table after the early repayment so you can visualise the new payoff date and the updated balance curve.

Frequently asked questions about reducing the term with early repayment

How can I cut years off my mortgage with early repayment?

Apply a partial prepayment aimed at reducing the term while keeping the instalment similar. The calculator shows the shorter duration, the new payoff date and the updated amortization chart so you can quantify the time and interest saved.

What is the difference between reducing the term and lowering the instalment?

Reducing the term keeps your instalment roughly the same but pays off the loan sooner, maximising interest savings. Lowering the instalment decreases the monthly outlay but keeps a longer schedule, which is why we offer another calculator specifically for reducing the payment.

Can I use the calculator for personal loans as well?

Yes. The simulator works with mortgages and personal loans alike, generating a new shorter term, the updated payoff date and the corresponding amortization table after the early repayment.